Banks and banking services were introduced to provide access to finance and the safekeeping of valuables.

The concept of banking in Ghana has gradually gained popularity over the years, with a significant increase in bank account ownership since 2013.

As of 2022, close to 50% of Ghana’s population had an account with a financial institution, and this has risen to a bank account penetration of 67.1%, with a debit card penetration of 18.5% among Ghanaians above 15 years of age.

However, despite this growth, customers of traditional banks have expressed dissatisfaction with the current banking system, demanding more from the services they receive. Let me share a personal experience from a conversation with Jeff (not his real name). He recounted his ordeal when he needed to withdraw cash using his debit card but faced issues with the available ATM. Despite being debited, he received no cash, and his card got stuck in the machine, leaving him stranded. When he approached the bank the next day, he was informed that it would take 60 days to reconcile with his own bank before he could get his deducted cash back. Such incidents contribute to the growing discontent among bank customers.

Beyond this, other common complaints include high maintenance costs, long queues at banking halls, and bureaucratic processes when seeking overdrafts or loans. Some individuals choose not to keep their money in banks due to concerns about the stability of banks, especially after the cleanup of the banking sector in Ghana from mid-2017 to January 2020, which resulted in the reduction of banks from 34 to 23, and the revocation of licenses from 347 microfinance institutions, 15 savings and loans, and 8 finance houses.

Results from a survey recently held to ascertain the level of satisfaction that bank customers were getting from their respective banks indicated that a majority of them wanted more than what was currently being offered. 90% of respondents, a healthy balance of males and females,

indicated that they each had more than one bank account and in addition made use of other financial apps apart from those of their banks. We’ve outlined the top 3 challenges these respondents faced from their banks;

Customer Service

A significant number of respondents expressed dissatisfaction with their bank's customer service, citing issues such as unresponsiveness and slow response times. Furthermore, customers highlighted a lack of timely communication and updates from their banks, fostering a perception of inadequate transparency. Another layer of frustration stemmed from bank customer service teams perceived to have insufficient knowledge and competence.

High Charges and fees for bank services

A major concern among respondents was the exorbitant charges and fees associated with bank services, including transaction fees and account maintenance charges. This discontent was particularly pronounced given recent upward revisions in monthly service charges, a move viewed unfavorably amid challenging economic conditions.

Unreliable Bank Technology

Respondents reported difficulties in even minor tasks, such as resetting bank app passwords, necessitating visits to crowded banking halls. The experience was compounded by the presence of glitchy bank apps, frequent downtimes, and persistent pending transactions. Adding to the frustration, users pointed out that transferring funds to other banks and mobile wallets through these apps was more complex compared to non-bank payment alternatives.

These grievances have eroded confidence in traditional banks, prompting Ghanaians to demand expanded services from financial institutions. These evolving expectations encompass insurance, online lending, investment consultancy, and financial management. Consequently, some banks are adapting by introducing services not traditionally associated with banking. The transformative wave is most evident with the entry of neobanks and fintech apps, which provide comprehensive financial services and a broader array of digital solutions. This shift responds to the growing demands of customers seeking enhanced and diversified financial offerings.

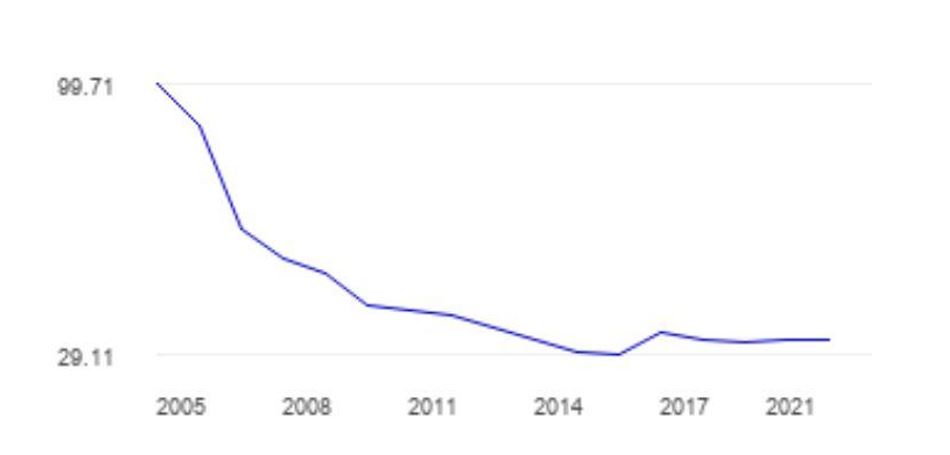

Graph for the decrease in active bank accounts in Ghana (2005 – 2021)

Neobanks and digital financial apps provide a solution to the challenges faced by traditional banks. They offer convenient access to funds without the need to visit a physical banking hall or use an ATM machine. In a rapidly evolving financial landscape, these digital platforms have proven themselves not only as effective means of transferring funds and making payments but also as reliable stores of value.

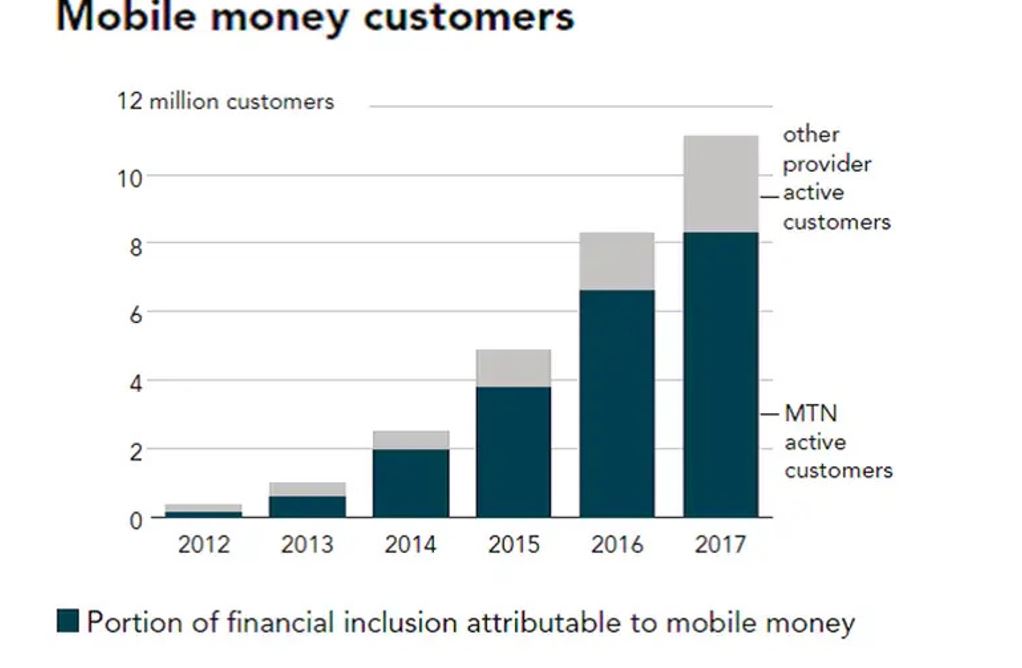

Graph for the Increase in Mobile Money Customers and Users (2012 – 2017)

As the use of mobile money wallets and fintech apps continues to rise, it prompts the question: Are digital apps becoming more reliable and innovative than traditional banks in Ghana? The shift towards these digital platforms raises the question of whether Ghanaian banks need to enhance their offerings to meet the evolving needs of the bankable public.

Could the future of money and payments in Ghana be in the hands of mobile payment systems? Ghanaians are seeking more, wanting more, and deserving more from our banks and bankers.

This article is by Yaw Addo (A finance and business content contributor / analyst)

Read Full Story

Facebook

Twitter

Pinterest

Instagram

Google+

YouTube

LinkedIn

RSS